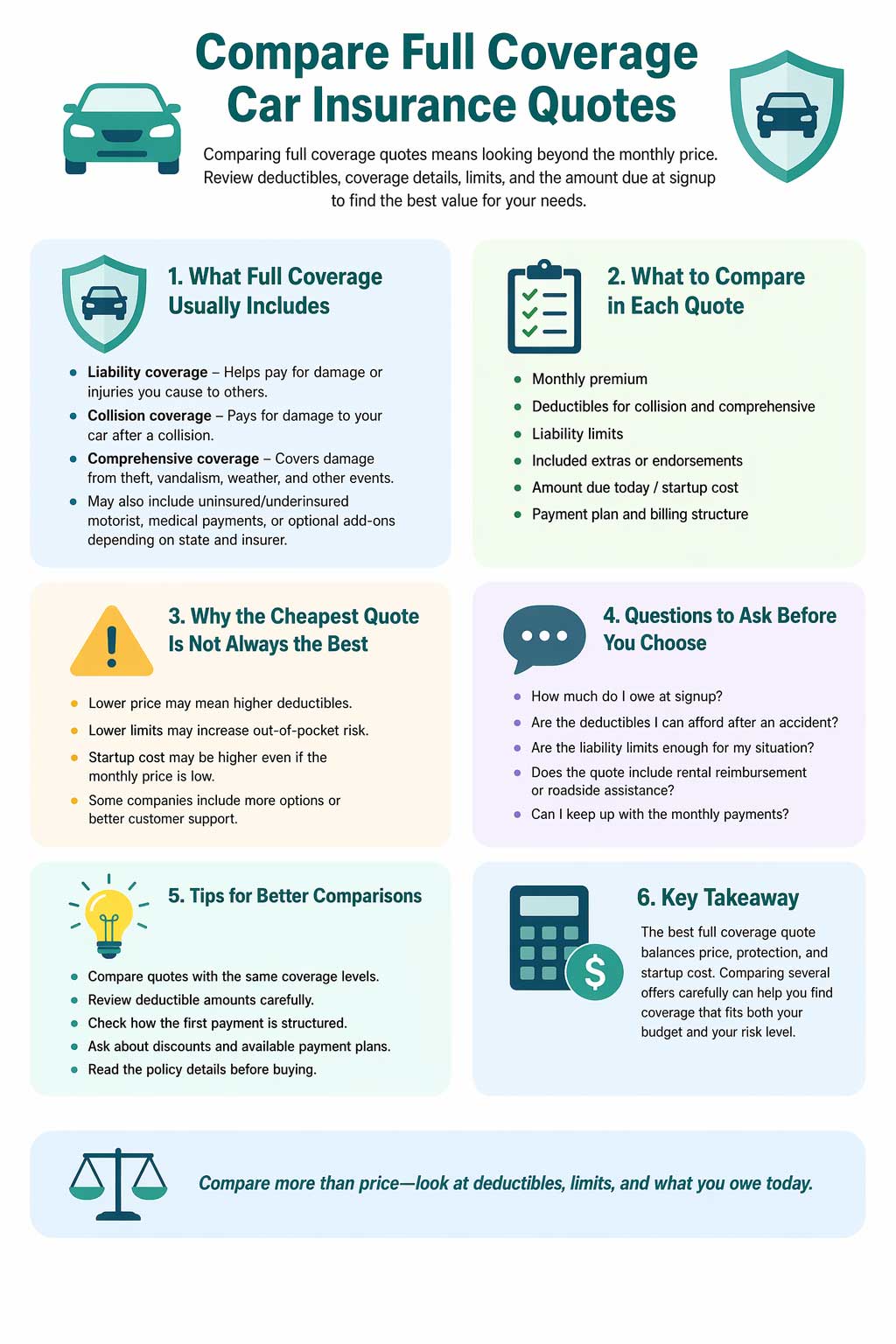

If you are shopping for full coverage car insurance, comparing quotes is one of the smartest ways to find a policy that fits your budget and still gives you the protection you need. A quote can look affordable at first glance, but the monthly premium alone does not tell the whole story.

That is because full coverage usually means more than just the state-required liability insurance. In many cases, it refers to liability plus collision and comprehensive coverage, along with any other required coverages in your state. Two quotes can look similar on price while offering very different deductibles, liability limits, and overall protection.

Quick Answer

To compare full coverage car insurance quotes effectively, look at more than just the monthly premium. Compare liability limits, deductibles, collision and comprehensive coverage, optional add-ons, and the amount due at signup. The cheapest quote is not always the best value if it leaves you underinsured or makes it hard to afford repairs after a claim [1] [2] [3].

What Full Coverage Usually Means

Full coverage is not an official insurance term in the same way liability, collision, or comprehensive are. It is usually a shorthand way of describing a policy that includes liability coverage plus protection for your own vehicle, especially collision and comprehensive [1] [2].

That matters because drivers often assume every full coverage quote includes the same thing. It does not. One insurer may quote lower liability limits, a higher deductible, or fewer extras than another. That is why comparison matters so much.

Why Comparison Matters

Two policies may both be described as full coverage, but one could have much higher deductibles or lower liability limits than the other. Always review the details before choosing based only on price.

What Full Coverage Usually Includes

Most drivers use full coverage to mean a policy built around three core parts:

- Liability coverage for injuries or property damage you cause to others

- Collision coverage for damage to your own car after a covered accident

- Comprehensive coverage for non-collision losses such as theft, vandalism, hail, fire, or animal damage

Some drivers also add uninsured motorist coverage, roadside assistance, rental reimbursement, or gap insurance. What is included varies by insurer, by state, and by the choices you make when the quote is built [2] [4].

What To Compare in Full Coverage Quotes

When comparing quotes, focus on the details that affect both your cost and your protection.

1. Liability Limits

Liability limits determine how much your insurer will pay if you injure someone or damage their property. State minimum limits may be low, and some insurers may quote only the minimum unless you ask for higher protection [5].

If one quote has much lower liability limits than another, it may look cheaper but leave you with more personal financial risk after a serious accident.

2. Collision and Comprehensive Deductibles

Your deductible is the amount you pay out of pocket before coverage helps with repairs. A higher deductible usually lowers the premium, but it also means you must pay more after a claim [3] [6].

For example, one quote may have a $500 deductible while another has a $1,000 deductible. The second quote could appear more affordable, but it may be harder to use when you actually need repairs.

3. Amount Due at Signup

If you are trying to manage your budget, compare not only the monthly price but also the upfront payment or startup cost. Some insurers require the first month, a deposit, or other fees before coverage begins. A quote with a lower monthly premium could still have a higher amount due today.

If keeping the initial cost low is important, you may also want to read low or no down payment car insurance.

4. Optional Coverages

Some quotes include extras such as roadside assistance or rental reimbursement, while others do not. These add-ons can make one quote look more expensive even though it offers more value. Make sure you are comparing similar coverage packages.

5. Exclusions and Policy Details

Not every policy works the same way. You should check whether the quote includes the protections you expect and whether there are limitations that affect your situation. For example, financed or leased vehicles often need broader protection because the lender may require collision and comprehensive [4].

Compare These Before You Buy

- Monthly premium

- Amount due today

- Liability limits

- Collision and comprehensive deductibles

- Optional add-ons

- Exclusions and restrictions

- Whether the policy fits your car and budget

Why the Cheapest Full Coverage Quote Is Not Always the Best

It is natural to look for the lowest price, but the cheapest full coverage quote is not always the best option. Some cheaper quotes have higher deductibles, lower liability limits, or fewer included features.

A lower premium may save money now, but it can cost more later if you have to pay more out of pocket after a claim or if your liability limits are too low for a serious accident. If your main goal is to keep this kind of policy affordable, see affordable full coverage car insurance.

When Full Coverage May Be Worth It

Full coverage is often worth comparing if:

- Your car is financed or leased

- Your vehicle still has significant value

- You could not easily afford to replace or repair the car yourself

- You want broader protection beyond state minimum liability

On the other hand, some older vehicles with very low market value may not justify the cost of collision and comprehensive coverage. The right choice depends on your budget, the value of your car, and how much risk you are comfortable taking [6] [7].

Tips To Compare Full Coverage Quotes More Accurately

Use the Same Driver and Vehicle Information

Make sure each quote is based on the same car, driver profile, annual mileage, garaging address, and driving history. Small differences in information can change the quote.

Choose Matching Coverage Levels

Compare quotes with the same liability limits and deductibles whenever possible. Otherwise, one quote may look cheaper simply because it provides less protection.

Check How Much You Owe Upfront

Always look at the amount due at signup, not just the monthly premium. This matters even more if you are trying to get insured quickly while keeping your initial payment manageable.

Review the Insurer’s Payment Options

Some insurers allow monthly billing or automatic payment discounts, while others may require a larger upfront payment. These details can affect how affordable the policy feels in real life.

Ask About Discounts

You may qualify for discounts based on safe driving, bundling, defensive driving courses, autopay, paperless billing, or vehicle safety features [6].

Common Mistakes When Comparing Full Coverage Quotes

- Looking only at the monthly premium instead of comparing total cost and amount due today

- Ignoring deductible differences between quotes

- Comparing different liability limits without noticing

- Overlooking excluded or optional coverages

- Assuming full coverage means the same thing everywhere

Full Coverage vs. Liability-Only

Liability-only insurance is usually cheaper because it covers damage you cause to others but does not usually pay to repair your own vehicle after an at-fault crash. Full coverage costs more because it adds collision and comprehensive protection [2] [7].

If you are deciding between policy types, you may also want to read cheap liability car insurance.

Can You Get Full Coverage With a Low Down Payment?

Sometimes yes, but it depends on the insurer, your driving history, the value of the vehicle, and your state. Full coverage tends to cost more than liability-only, so the amount due upfront may also be higher. Comparing quotes can help you identify insurers that offer more manageable startup costs.

If quick coverage is important, see same-day car insurance.

Who Should Compare Full Coverage Quotes Carefully?

Comparing quotes is especially important if you:

- Have a financed or leased vehicle

- Need a policy that fits a tight budget

- Want to lower the amount due today

- Have a newer or higher-value car

- Need to balance protection with affordability

Key Takeaway

To compare full coverage car insurance quotes effectively, focus on coverage details, deductibles, liability limits, optional coverages, and the amount due at signup, not just the monthly price. A slightly higher premium may offer better protection or a more realistic deductible, while the cheapest quote may leave important gaps.

Final Thoughts

Comparing full coverage car insurance quotes carefully can help you find a policy that fits both your budget and your real-world needs. The best quote is not always the one with the lowest premium. It is the one that gives you the level of protection you actually need at a cost you can realistically maintain.

If your goal is to protect your vehicle as well as your finances, it is worth taking a few extra minutes to compare the details instead of choosing only by price.

References

- Progressive – What Is Full Coverage Car Insurance? ↩ Back to section

- Progressive – Liability vs. Full Coverage Car Insurance ↩ Back to section

- NAIC – Comparing Online Auto Insurance Quotes ↩ Back to section

- NAIC – Does Your Vehicle Have the Right Protection? ↩ Back to section

- NAIC – A Consumer’s Guide to Auto Insurance ↩ Back to section

- Insurance Information Institute – Nine Ways to Lower Your Auto Insurance Costs ↩ Back to section

- Insurance Information Institute – What Is Covered by Collision and Comprehensive Auto Insurance? ↩ Back to section