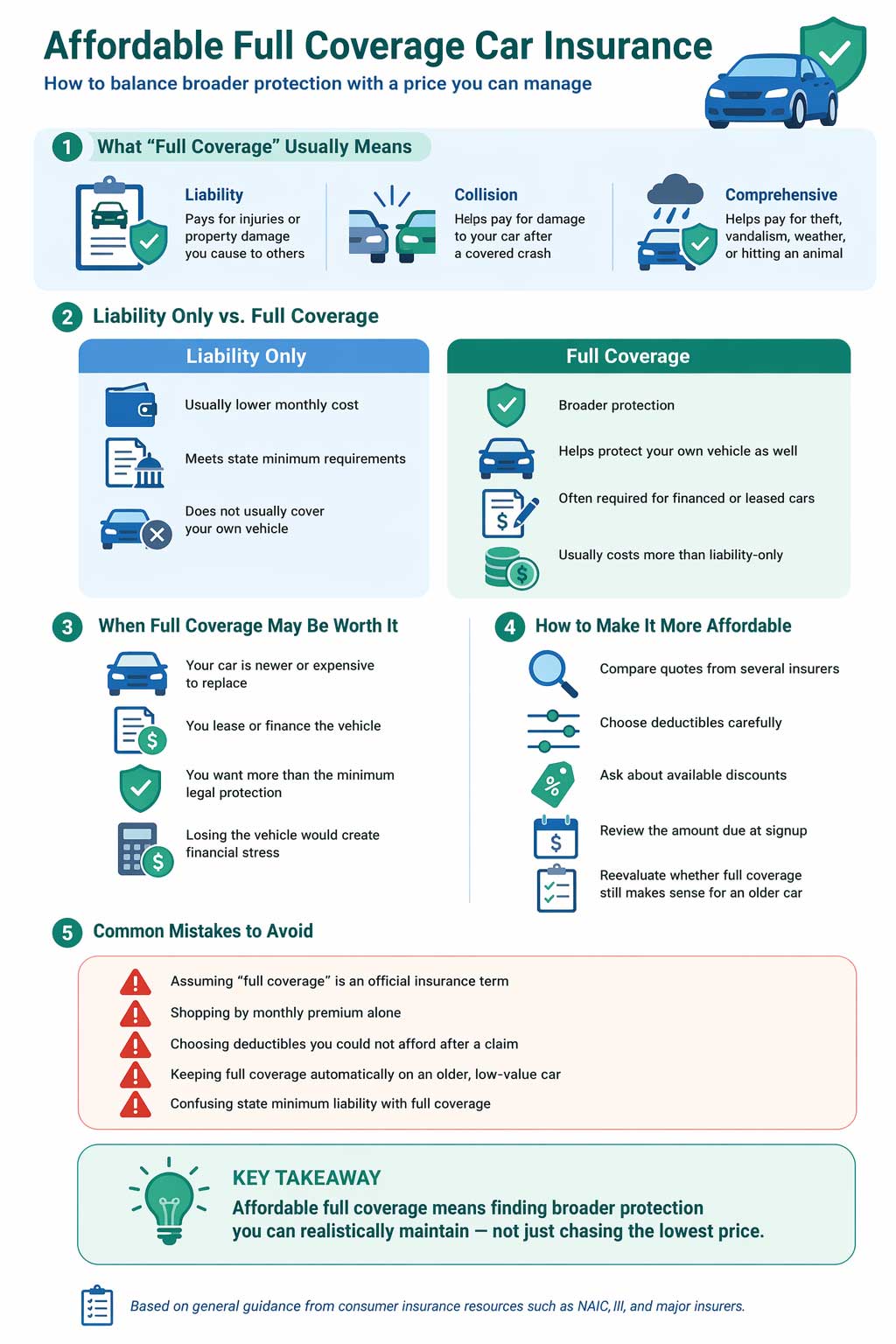

Many drivers search for no down payment car insurance because they need coverage now and want to avoid a large amount due upfront. But the number that matters most is not always what you pay today. It is the total cost of the policy over time.

That distinction matters because a lower first payment can still lead to a more expensive policy overall. A quote with a smaller amount due at signup may come with higher monthly payments, fewer discounts, a less favorable billing structure, or coverage choices that cost more across the full policy term.

Quick Answer

The total cost of no down payment car insurance is usually the full amount you pay over the policy term, not just the first payment. In practice, reputable zero-down auto insurance usually does not exist. What drivers normally find is a lower initial payment, followed by later installments that still add up to the full premium [1] [2].

What Total Cost Actually Means

When drivers compare no down payment car insurance options, they often focus on the amount due today. But the total cost is broader than that. It usually includes the full premium across the policy term, whether you pay monthly, every six months, or in full at the start [1] [3].

That is why a quote with a smaller startup payment is not automatically the cheapest quote overall. If one insurer lets you start with less cash but charges more over time, the low down payment option may end up costing more by the end of the policy.

Why No Down Payment Usually Does Not Mean Zero Total Cost

Reputable no down payment car insurance usually does not mean truly free coverage at the start. Progressive states directly that reputable zero-down auto insurance does not really exist and that the money due upfront is typically part of the total premium, not a separate fee [1]. In other words, the first payment is only one part of the bill.

That means the real question is not, “Can I pay nothing today?” It is, “What will this policy cost me in total, and can I realistically keep paying it?”

If you want the broader explanation of the phrase itself, also read what no down payment car insurance really means.

Why a Lower First Payment Can Still Cost More Overall

A lower first payment can feel like a win, especially when cash is tight. But it can sometimes come with tradeoffs that raise the total policy cost over time. Common examples include:

- higher monthly installments

- fewer paid-in-full discounts

- fees or less favorable billing structures

- coverage choices that keep the deductible low but push the premium higher

Some insurers also offer discounts when you pay the premium in full up front, and some payment plans require only a percentage of the premium at the start and split the rest across later installments [4] [5] [6]. That means two drivers can see very different amount due today numbers even when the total premium is similar.

What Drives the Total Cost of a Policy

The total cost of car insurance is shaped by more than billing. The Insurance Information Institute and NAIC both explain that auto premiums are affected by things like the type and amount of coverage, policy limits, deductibles, and rating factors tied to the driver and vehicle [7] [8].

Some of the biggest cost drivers include:

- the liability limits you choose

- whether you buy collision and comprehensive

- the deductible amount

- your driving record

- your ZIP code and state

- the vehicle itself

- whether discounts apply

That is why two no down payment style quotes can end up very different in total cost even if the startup payment looks similar.

How Deductibles Affect the Bigger Picture

One of the most overlooked pieces of total cost is the deductible. NAIC and III both note that higher deductibles usually lower your premium, while lower deductibles usually raise it [8] [9]. That can make a policy look more affordable month to month if you accept more out-of-pocket risk after a claim.

So when comparing no down payment options, do not ask only, “How much do I owe today?” Also ask, “How much will I pay over time?” and “Could I handle this deductible if I need to use the policy?”

How To Compare Total Cost More Accurately

If your real goal is lower overall spending, compare policies using the same coverage setup and then look at the full payment structure.

1. Compare the full premium, not just the first payment

The startup amount matters, but it is only part of the total bill.

2. Check whether paying in full changes the price

Some insurers offer a pay-in-full discount, which can reduce the total cost even if the initial outlay is higher [4] [5].

3. Compare the same deductibles and limits

If one quote has lower deductibles or higher liability limits, it may cost more for good reason [8] [9].

4. Ask about discounts

Paperless billing, autopay, safe driving, and other discounts can change the real cost of a policy [4] [10].

5. Think about the policy term, not just one month

A policy that feels cheap at the start can become expensive if the monthly payments are hard to maintain.

If you are comparing broader policies too, see compare full coverage car insurance quotes. If you mainly want the cheapest basic option, see cheap liability car insurance.

Who This Page Helps Most

This page is especially useful if you:

- care more about long-term affordability than just the first payment

- are trying to understand whether low down payment really saves money

- want to compare monthly billing against paying in full

- need coverage now but do not want a misleadingly cheap-looking quote

Common Mistakes To Avoid

- Confusing the first payment with the total premium: they are not the same [1] [3].

- Ignoring deductibles: lower deductibles can raise the premium [8] [9].

- Comparing different coverage setups: that can make one quote look cheaper unfairly.

- Missing discount opportunities: billing and payment choices can matter [4] [10].

- Choosing a payment plan you cannot maintain: a lapse can make future insurance harder to manage.

Key Takeaway

No down payment car insurance total cost is about the full financial picture, not just what is due at signup. A lower first payment can help in the short term, but the better value often comes from comparing the full premium, deductibles, discounts, and payment structure together.

Frequently Asked Questions

Does no down payment car insurance really reduce my total cost?

Not automatically. In many cases, it lowers the amount due at the start but does not reduce the full premium you owe over the policy term [1] [2].

Is the first payment separate from the premium?

Usually no. Progressive explains that the down payment is typically part of the total premium, not a separate fee [1].

Can paying in full lower the total cost?

Sometimes yes. Some insurers offer discounts for paying the policy in full up front [4] [5].

Do higher deductibles lower the premium?

Usually yes. NAIC and III both note that higher deductibles generally lower premiums, while lower deductibles usually increase them [8] [9].

What if I mainly need coverage today?

Then your best next page may be same-day car insurance, especially if speed matters more than long-term cost analysis.

Final Thoughts

No down payment car insurance total cost is one of the most important ideas to understand before you buy. The startup payment matters, but it does not tell you whether the policy is truly affordable over time.

The best comparison is usually the one that shows what you owe today, what you will owe later, what discounts apply, and whether the deductible and coverage choices still make sense for your situation.

Compare the Full Cost, Not Just the First Payment

Start with the page that fits your situation, review how low upfront payments work, and compare total policy cost before choosing the quote that only looks cheapest at the start.

References

- Progressive – Can I Get Car Insurance With No Down Payment? ↩ Back to section

- ValuePenguin – Cheap No Down Payment Car Insurance ↩ Back to section

- Progressive – What Is a Car Insurance Premium? ↩ Back to section

- Progressive – Car Insurance Discounts ↩ Back to section

- GEICO – 11 Ways to Save on Car Insurance ↩ Back to section

- GEICO – Car Insurance Payments: Methods and Plans ↩ Back to section

- Insurance Information Institute – What Determines the Price of an Auto Insurance Policy? ↩ Back to section

- NAIC – A Consumer’s Guide to Auto Insurance ↩ Back to section

- Insurance Information Institute – Understanding Your Insurance Deductibles ↩ Back to section

- GEICO – 10 Effective Ways to Lower Your Car Insurance Rate ↩ Back to section