If your auto insurance lapsed and you need coverage again fast, the biggest challenge is usually the upfront cost. Many drivers in this situation are not looking for a perfect policy first. They are looking for a practical way to get insured again without a large initial payment.

That is where low down payment car insurance can help. While true zero-down policies are uncommon, many drivers can still find options with a smaller first payment, especially if they compare quotes carefully, choose only the coverage they need right now, and act before the lapse turns into a longer uninsured period.

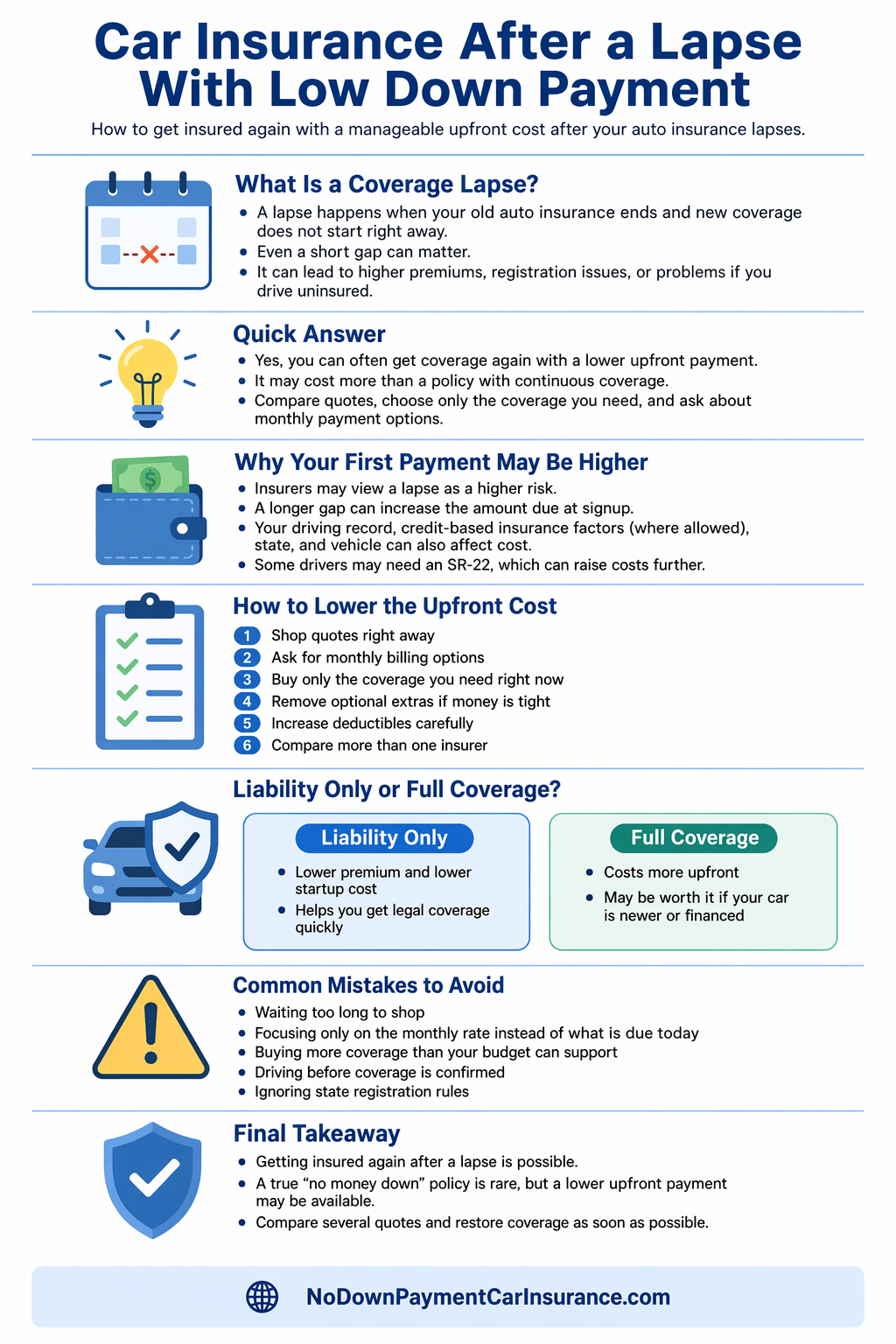

Quick Answer

Yes, you can often get car insurance after a lapse with a lower upfront payment, but it may cost more than a policy with continuous coverage. The best strategy is to compare quotes quickly, ask about monthly payment options, avoid unnecessary extras, and choose the right level of coverage for your current situation.

What Counts as a Car Insurance Lapse?

A lapse happens when your previous auto insurance ends and your new coverage does not begin immediately. Even a short gap can matter. For insurers, a lapse may suggest added risk. For drivers, it can create legal and financial problems if the vehicle remains registered or is driven while uninsured [1].

Not every lapse starts the same way. Some happen because a payment was missed. Others happen after a cancellation, a move to a new state, a change in vehicle ownership, or a simple delay in renewing a policy. In real life, many drivers do not notice the gap until they try to buy coverage again and see a higher quote.

This is why timing matters. If your policy recently ended, it usually makes sense to shop for replacement coverage immediately instead of waiting. A shorter lapse is often easier to explain and easier to recover from than a longer uninsured history [5].

Can You Really Get Low Down Payment Car Insurance After a Lapse?

Yes, in many cases you can. The key is understanding what low down payment really means. It usually does not mean free coverage. It usually means the insurer allows you to start the policy with a smaller first payment instead of paying a large percentage of the premium upfront [4].

That distinction matters. Some drivers search for “no money down” because they need insurance today, but what they actually need is a policy structure with manageable startup costs. If you want a broader explanation of how that works, see what no down payment car insurance really means.

After a lapse, some companies may ask for a higher initial payment because the gap in coverage increases perceived risk. Others may still offer monthly billing with a relatively modest first installment. That is why shopping around matters so much here. Two insurers can look at the same driver and price the first payment very differently [5].

Why the Down Payment May Be Higher After a Lapse

Drivers are often surprised that the main problem is not just the total premium. It is the amount due today. After a lapse, the insurer may decide that a larger first payment helps offset the risk of insuring a driver who recently went without coverage.

Several factors can push that first payment up:

- How long the lapse has lasted

- Your driving record

- Your credit-based insurance characteristics where allowed

- Whether you need an SR-22

- The type of car you drive

- The amount of coverage you choose

- Your state and ZIP code

This is one reason why two people can both search for low down payment insurance and get very different results. The lapse is only one piece of the picture. The car, the coverage level, and the driver profile can all affect the startup cost.

How to Get Insured Again Without a Huge Upfront Payment

The first goal is simple: get back into continuous coverage as soon as possible. The second goal is to keep the first payment manageable. The steps below usually give drivers the best chance of doing both.

1. Shop quotes right away

The longer you wait, the harder the lapse can be to explain away. Start comparing quotes as soon as you know the previous policy ended or is about to end. Speed matters here [5].

2. Ask about monthly billing options

Some insurers or agencies can structure the policy with a smaller amount due at signup and the rest spread across future installments. Always ask what is due today, not just what the monthly premium looks like on paper.

3. Buy only the coverage you need right now

If cash is tight, focus first on legal compliance and immediate protection. Depending on your situation, you may decide to start with liability-only coverage and upgrade later. If your vehicle is financed, remember that the lender may require broader coverage [1].

4. Remove optional extras that are not essential

Roadside assistance, rental reimbursement, and similar add-ons can be useful, but they also increase the amount due. If the priority is restarting coverage, you can keep the policy lean and review those extras later.

5. Increase deductibles carefully

For drivers buying collision or comprehensive coverage, a higher deductible can lower the premium. Just make sure the deductible is still realistic for your budget if you have a claim.

6. Compare specialized and standard markets

Some companies are more flexible than others with recent lapses, higher-risk profiles, or unusual billing situations. That is one reason it helps to compare more than one company instead of applying to only the first one you find.

Should You Choose Liability Only or Full Coverage?

This is one of the most important decisions for drivers trying to restart insurance after a lapse. If your main issue is affordability, liability-only coverage may be the easiest path back into compliance because it usually has a lower premium and a lower startup payment.

That said, cheaper is not always better. If you drive a newer vehicle, owe money on the car, or cannot afford to replace it after a crash, liability-only coverage may leave a serious gap. In that case, you may still want broader protection even if the first payment is higher.

If you are trying to compare the lower-cost side of the market first, you can also review cheapest car insurance with low down payment. If you want to compare provider types, see best low down payment car insurance companies.

How to Improve Your Chances of a Smaller First Payment

There is no guaranteed trick that works for every driver, but these moves often help:

- Choose the shortest possible gap between your old and new policy

- Keep the same vehicle if changing cars would raise the quote

- Ask whether paperless or automatic payments lower the bill

- Bundle where it makes sense, especially if you already have renters or home insurance

- Review your coverage limits to avoid paying for more than you need today

- Correct application errors, including garaging address, mileage, and driver history details

It also helps to be realistic. If your lapse is combined with an SR-22 requirement, recent accidents, tickets, or very poor credit-based insurance factors where permitted, the first payment may still be higher than you want. In that situation, the win is often getting active coverage again now and improving the profile over time.

Common Mistakes to Avoid After a Lapse

Many drivers make the same errors when trying to fix a lapse quickly. Avoiding them can save both money and time.

- Waiting too long to shop: a short lapse is usually easier to recover from than a long one.

- Focusing only on the advertised monthly rate: the amount due today is what matters most when cash is tight.

- Buying more coverage than your current budget can support: a policy only helps if you can keep it active.

- Driving before coverage is confirmed: never assume you are insured until the policy is active.

- Ignoring state or registration rules: if the vehicle is still registered, the lapse can trigger extra problems depending on your state [3].

For drivers who need coverage urgently, this is also where same day car insurance becomes relevant. Same-day activation and low upfront cost are not the same issue, but they often overlap after a recent lapse.

When a Recent Lapse May Still Be Fixable

If you missed a payment only a few days ago, contact the insurer or agency immediately. In some cases, a policy may still be within a notice period or grace period, and reinstating the existing policy could be easier than shopping for a completely new one. That is not guaranteed, and the rules vary by insurer and by state, but it is often worth checking before starting over from scratch [2].

If reinstatement is no longer available, then the goal shifts to finding a new active policy as soon as possible and avoiding any further delay. Even when the first quote looks high, comparing more carriers can still make a meaningful difference.

Who This Page Is Really For

This page is especially useful for drivers who recently missed a payment, had a cancellation, switched vehicles, moved, or let coverage expire while trying to save money. It is also relevant for people who are now searching phrases like “cheap car insurance after lapse,” “insurance after cancellation,” or “how to get insured again fast with low down payment.”

In other words, this is not just another version of a general no-down-payment page. It is for a driver with a specific problem: coverage stopped, money is tight, and the next step needs to be practical.

Frequently Asked Questions

How long does a lapse affect car insurance quotes?

That depends on the insurer, the state, and the length of the gap. In general, a recent lapse can affect what you pay when you shop again, especially if the gap is more than just a few days [5].

Can I get same-day coverage after a lapse?

Often yes. Many insurers can start a policy quickly once payment is made and the application is approved. The bigger question is usually how much is due upfront.

Is low down payment insurance the same as no down payment insurance?

Not exactly. In practice, many offers marketed as no down payment still require some money upfront, often the first month or another initial installment [4].

Will a lender care if my insurance lapses?

Yes, if the vehicle is financed. A lender may require continuous physical damage coverage and could take steps to protect its interest if your policy lapses [1].

Should I cancel registration if I am not driving the car?

That depends on your state rules. In some states, you may need to notify the DMV or take non-use steps to avoid registration problems if the vehicle remains uninsured [3].

Final Thoughts

Getting car insurance after a lapse with low down payment is possible, but it usually takes more comparison and more attention to the first payment than drivers expect. The best move is to act quickly, compare several quotes, and build a policy that fits your budget now while helping you reestablish continuous coverage.

If you are dealing with a recent gap, do not get stuck chasing the idea of perfect zero-down coverage. Focus on what is realistic: a manageable startup payment, active insurance today, and a policy you can keep in force going forward.

References

- National Association of Insurance Commissioners (NAIC) – A Consumer’s Guide to Auto Insurance ↩ Back to section

- Progressive – Car Insurance Lapse & Grace Periods Explained ↩ Back to section

- California DMV – Suspended Registration Reinstatement ↩ Back to section

- ValuePenguin – Cheap No Down Payment Car Insurance ↩ Back to section

- The Zebra – Car Insurance with a Lapse in Coverage ↩ Back to section