If you drive but do not own a car, you may still need insurance. That is where non-owner car insurance comes in. For many drivers, the appeal is simple: get liability protection without paying for a full standard auto policy tied to a specific vehicle.

If your budget is tight, the next question is usually whether you can get non-owner car insurance with a low down payment. In many cases, yes. But just like other “no down payment” searches, the real answer is usually about finding a smaller first payment rather than truly starting coverage for free [5].

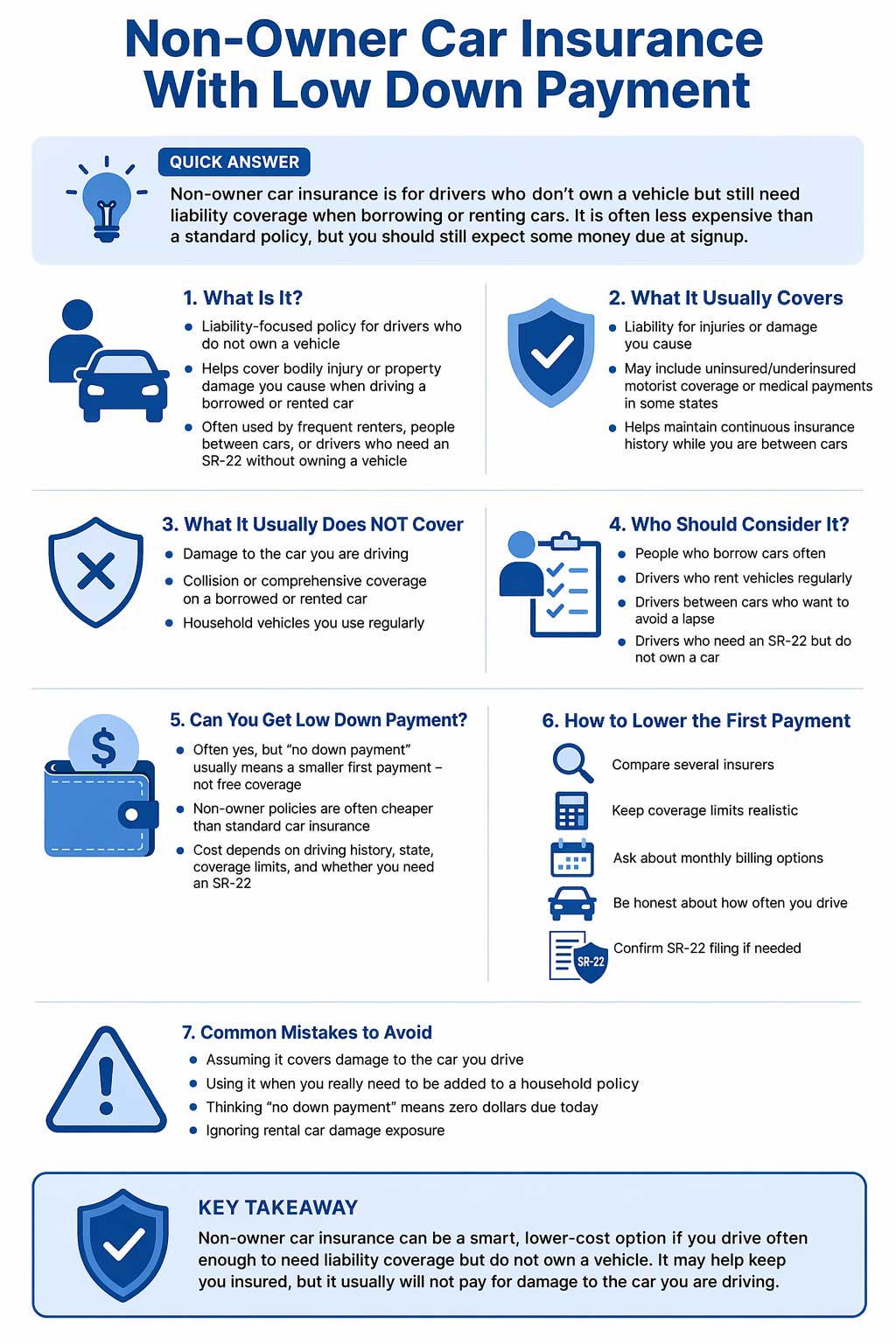

Quick Answer

Non-owner car insurance is designed for drivers who do not own a vehicle but still need liability coverage when they borrow, rent, or sometimes use shared cars. It is often less expensive than a standard auto policy, but it usually does not cover damage to the vehicle you are driving. A low down payment may be possible, but you should expect at least some money due at signup [2] [5].

What Is Non-Owner Car Insurance?

Non-owner car insurance is a liability-focused policy for someone who drives but does not own a vehicle. Instead of insuring a specific car, the policy mainly covers you as the driver when you cause bodily injury or property damage while driving a car you do not own [2] [3].

This type of policy is often used by people who regularly borrow cars, rent vehicles, or want to maintain continuous insurance coverage even while they do not currently own a car. It can also be useful for drivers who need proof of insurance for an SR-22 filing even though they do not own a vehicle [4] [6].

If you are still comparing how low upfront payment insurance works in general, you can also read what no down payment car insurance really means.

What It Usually Covers

The main purpose of non-owner insurance is liability protection. If you cause an accident while driving a borrowed, rented, or sometimes shared vehicle, the policy may help cover the other party’s injuries or property damage up to your policy limits [2] [3].

Depending on the insurer and your state, a non-owner policy may also offer optional protections such as uninsured or underinsured motorist coverage, medical payments coverage, or personal injury protection. Availability varies, so you should confirm exactly what is included before buying [2].

That matters because many drivers assume non-owner insurance is just “cheap coverage without a car.” In reality, it is a specific liability product. It can be practical and affordable, but it is not the same thing as a full policy on a vehicle you own.

What It Usually Does Not Cover

This is where many drivers get confused. Non-owner insurance typically does not cover damage to the car you are driving. It also generally does not give you collision or comprehensive protection for that borrowed or rented vehicle, which means it is not a substitute for every type of rental car protection or for a full standard auto policy [2] [3].

If you rent cars often, this distinction matters. A non-owner policy can help with liability, but you may still need collision damage protection from the rental company or another source for physical damage to the rental car [2] [3].

It also usually is not the right solution if you own a car, live with someone whose car you regularly use, or need coverage for a household vehicle you access all the time. In those cases, insurers often expect you to be listed on the vehicle owner’s policy instead [2] [6].

Who Should Consider Non-Owner Insurance?

Non-owner insurance may make sense if you do not own a vehicle but you still drive often enough that being uninsured would create risk. Common examples include:

- Drivers who frequently borrow a friend’s or relative’s car

- People who rent vehicles regularly

- Drivers who use car-sharing services often

- People who want to avoid a lapse in insurance history while they are between cars

- Drivers who need an SR-22 filing but do not currently own a vehicle

It can also be a practical bridge policy if you recently sold your car and plan to buy another one later. In that situation, keeping some form of insurance in place may help you avoid a gap that could make future coverage more expensive. If that sounds like your situation, you may also want to read car insurance after a lapse with low down payment [6].

When It Is Not a Good Fit

Non-owner insurance is not for everyone. In many cases, it is the wrong product if:

- You already own a car

- You regularly drive a car owned by someone in your household

- You only borrow or rent cars a few times per year

- You need coverage for damage to a vehicle you use often

That last point is important. Some drivers shop for non-owner insurance because it sounds cheaper, but cheaper does not help if it is the wrong coverage for how you actually drive. If you regularly use the same household car, trying to force a non-owner policy into that situation can create coverage problems later [2] [6].

Can You Get Non-Owner Car Insurance With Low Down Payment?

Often yes, but the same rule applies here as with other low-down-payment insurance pages: you should think in terms of a smaller first payment, not truly free coverage. Many “no down payment” offers in auto insurance still require an initial installment, first month, or other amount due at the start [5].

Because non-owner insurance usually provides liability-focused coverage and does not insure a specific vehicle, it is often less expensive than a standard policy. That can make the startup payment more manageable for some drivers, especially if they compare multiple companies and keep their coverage limits realistic for their budget [2] [3] [6].

Still, there is no guarantee the first payment will be low. Your rate may be affected by:

- Your driving history

- Your state and ZIP code

- The liability limits you choose

- Whether you need an SR-22 or FR-44 filing

- How often you are expected to drive

If your main goal is to compare lower-startup-cost policies in general, you can also look at low or no down payment car insurance and cheapest car insurance with low down payment.

Can You Get an SR-22 Without Owning a Car?

Yes. In many states, drivers who need an SR-22 after a serious violation can meet that requirement with a non-owner policy if they do not own a vehicle. The filing rules and required coverage limits vary by state, but non-owner SR-22 insurance is a real option for drivers who need proof of financial responsibility without buying coverage on a car they do not own [4].

This is one of the strongest use cases for a non-owner policy. A driver who lost a license, had a DUI, or was cited for driving without insurance may need to get back into legal driving status before buying a vehicle. A non-owner SR-22 policy can help fill that gap while keeping costs lower than a full standard auto policy in many cases [4] [6].

How to Get a Lower First Payment

If the goal is to keep startup costs down, these steps usually help:

1. Compare several insurers

Not every company offers non-owner insurance, and not every company prices it the same way. Comparing several options can make a noticeable difference [2] [6].

2. Keep coverage limits realistic but responsible

Higher limits usually cost more, but bare-minimum coverage can leave you exposed. Choose limits that fit both your budget and your real risk.

3. Ask about billing structure

Even when the total premium is not extremely low, some insurers may allow a smaller amount due at signup with future installments rather than a heavy first payment all at once.

4. Be honest about how often you drive

Non-owner insurance is meant for drivers who do not own a car. Giving inaccurate information about your access to vehicles, household drivers, or driving frequency can create problems later.

5. Ask specifically about SR-22 filing if needed

If you need proof of insurance for the DMV or court-related requirements, confirm the insurer can file the form in your state before you buy [4] [6].

Common Mistakes to Avoid

Many drivers misunderstand what non-owner insurance does. These are the most common mistakes:

- Assuming it covers damage to the vehicle you drive: in most cases, it does not [2] [3].

- Buying it when you really need to be added to a household policy: this can happen when you regularly use a spouse’s, partner’s, or roommate’s car [2] [6].

- Thinking “no down payment” means zero dollars due today: usually it means a lower initial payment, not free coverage [5].

- Ignoring rental car damage exposure: liability is not the same as protecting the rental vehicle itself [2] [3].

- Skipping the policy because you are temporarily without a car: a non-owner policy can sometimes help maintain continuous insurance history [3] [6].

Key Takeaway

Non-owner car insurance can be a smart low-cost solution when you drive often enough to need liability coverage but do not own a vehicle. The key is understanding its limits: it may help protect you from liability claims, but it usually will not pay for damage to the car you are driving.

Frequently Asked Questions

Is non-owner car insurance cheaper than regular car insurance?

Often yes. Because it usually provides liability-focused coverage and does not insure a specific vehicle, it is commonly less expensive than a standard policy, although your actual rate still depends on your history, limits, and state [2] [3] [6].

Can I get non-owner insurance with no car at all?

Yes. That is exactly what the product is designed for: drivers who do not own a car but still need insurance protection while driving vehicles they do not own [2].

Does non-owner insurance cover rental cars?

It may help with liability when you rent, but it usually does not cover physical damage to the rental vehicle itself. You may still need collision damage protection from the rental company or another source [2] [3].

Can I use non-owner insurance if I live with someone who has a car?

Usually that is not the best fit if you regularly use that person’s vehicle. In many situations, insurers expect household drivers to be listed on the owner’s policy instead [2] [6].

Can non-owner insurance help me avoid a lapse?

It can in some situations. Drivers between cars sometimes buy a non-owner policy to keep continuous insurance history while they are temporarily without a vehicle [3] [6].

Final Thoughts

Non-owner car insurance with low down payment can make sense if you drive often enough to need liability protection but do not own a vehicle. It is especially useful for renters, frequent borrowers, drivers between cars, and people who need SR-22 proof without buying a standard policy on a car.

The most important thing is buying it for the right reason. If you need coverage for damage to a car you use regularly, this may be the wrong product. But if you truly need liability coverage without vehicle ownership, a non-owner policy can be a practical and often lower-cost way to stay insured.

Compare Practical Low Down Payment Options

If you are deciding between a non-owner policy and other lower-cost coverage options, compare provider types, startup costs, and how much protection you actually need before you buy.

References

- National Association of Insurance Commissioners (NAIC) – Auto Insurance Consumer Guide ↩ Back to section

- Progressive – What Is Non-Owner Car Insurance? ↩ Back to section

- GEICO – Understanding Non-Owner Car Insurance ↩ Back to section

- Progressive – Non-Owner SR-22 Insurance ↩ Back to section

- ValuePenguin – Cheap No Down Payment Car Insurance ↩ Back to section

- ValuePenguin – Non-Owner Car Insurance: What Is It and Who Should Have It? ↩ Back to section