If you want stronger protection without paying more than your budget can handle, affordable full coverage car insurance is usually the goal. Many drivers are not looking for the absolute cheapest policy. They are looking for a practical balance between broader protection and a payment structure they can still manage.

That balance matters because full coverage usually means more than just the state-required liability insurance. It commonly refers to liability plus collision and comprehensive coverage, along with any other required coverages in your state [1] [2]. That broader protection can be worth it, but it also costs more than a liability-only policy in many cases [3] [4].

Quick Answer

Affordable full coverage car insurance usually means a policy that includes liability, collision, and comprehensive coverage at a price you can reasonably maintain. The smartest goal is not simply cheap full coverage, but full coverage with limits, deductibles, and startup costs that fit your real situation [1] [5] [6].

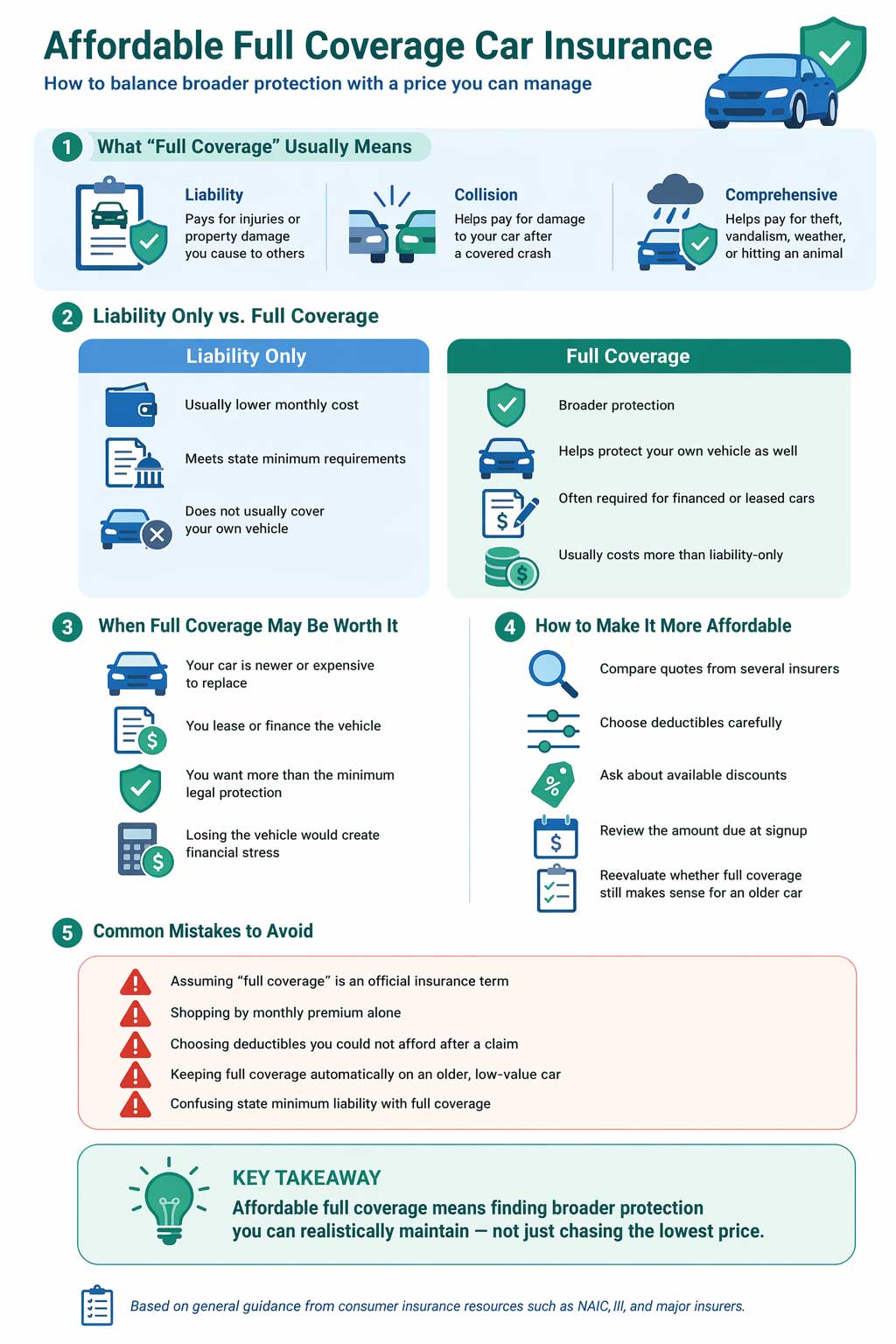

What Full Coverage Usually Means

Full coverage is not an official insurance term in the same way liability, collision, or comprehensive are. It is usually a shorthand way of describing a policy that combines liability coverage with physical damage protection for your own vehicle, especially collision and comprehensive [1] [2].

That is important because different drivers use the phrase differently. Some people mean everything legally required plus collision and comprehensive. Others assume it includes every possible protection, which is not always true. The safest way to think about it is this: full coverage usually means broader protection than liability-only, but you still need to verify exactly what the policy includes.

What It Usually Covers

An affordable full coverage policy still aims to protect more than the bare minimum. Common pieces of that broader setup include:

- Liability coverage: pays for injuries or property damage you cause to others

- Collision coverage: helps pay for damage to your own vehicle after a covered collision, usually minus your deductible

- Comprehensive coverage: helps pay for damage from non-collision events such as theft, vandalism, weather, fire, or hitting an animal, usually minus your deductible

That combination is why many drivers prefer full coverage when the vehicle is newer, financed, leased, or simply too expensive to replace out of pocket [3] [4] [5].

When Full Coverage Often Makes Sense

Affordable full coverage is usually most worth considering when the car would be difficult to replace if it were stolen, badly damaged, or totaled. It can also make more sense if your lender requires collision and comprehensive because the vehicle is financed or leased [4] [5].

In contrast, if you drive an older car with limited value, a broader policy may not always be the most efficient use of your money. That does not mean full coverage is wrong. It just means affordability should be measured against the vehicle’s value and your ability to absorb a loss.

Why Full Coverage Can Feel Expensive

Full coverage usually costs more because the insurer is taking on more potential loss. Instead of only paying for damage you cause to others, the policy may also pay for damage to your own vehicle from covered collisions and non-collision events [3] [4].

That cost can be pushed even higher by:

- the make, model, and value of the vehicle

- your age and driving record

- your ZIP code and state rules

- your deductibles

- recent claims or lapses

- credit-related insurance factors where allowed

If your main issue is weak credit or a recent gap in coverage, you may also want to read bad credit car insurance with low down payment and car insurance after a lapse with low down payment.

How to Make Full Coverage More Affordable

The goal here is not to strip the policy down until it barely protects you. The goal is to reduce cost intelligently while keeping the coverage useful.

1. Compare several insurers

Shopping around is still one of the most effective ways to control costs. Two insurers can price the same driver very differently [6].

2. Raise deductibles carefully

Higher deductibles on collision and comprehensive can lower your premium, but only if you can realistically afford that deductible after a claim [7] [8].

3. Review whether the car still justifies full coverage

On older vehicles, carrying collision and comprehensive may not always be cost-effective. The III and NAIC both note that reducing or dropping physical damage coverages on older vehicles can sometimes lower costs, unless a lender still requires them [7] [8].

4. Check the amount due at signup

The cheapest-looking monthly price is not the whole story. The amount due today matters too, especially if you are trying to start coverage with limited cash available.

5. Look for discounts that fit your situation

Bundling, safe driving, vehicle safety features, and other discounts can matter. Ask what is available instead of assuming the first quote already reflects everything [7].

If you want the broader lower-upfront-cost angle, start with low or no down payment car insurance. If your main priority is speed, see same-day car insurance.

Why State Minimums and Full Coverage Are Not the Same

Drivers often hear full coverage and assume it just means carrying enough insurance to be legal. That is not the same thing. State minimums usually refer to the minimum liability limits required to drive legally, and the NAIC warns that those minimums may not be enough to fully protect you and your assets after a serious accident [6].

That is one reason some drivers move beyond minimum liability and into a fuller policy structure. They are not only trying to comply with the law. They are trying to protect both their finances and their vehicle more effectively.

Who Affordable Full Coverage Fits Best

Affordable full coverage may be a smart target for drivers who:

- have a newer vehicle

- lease or finance their car

- would struggle to replace the car after theft or a major loss

- want broader protection but still need to control cost

It may be less attractive for drivers who:

- own an older car with low market value

- can absorb the loss of the vehicle more easily

- mainly want the lowest-cost legal option and accept the tradeoffs

If the cheaper side of the market matters more than protecting your own car, your better starting page may be cheap liability car insurance.

Common Mistakes to Avoid

- Assuming full coverage is a formal insurance term: it usually is not [1].

- Buying only by monthly premium: startup cost still matters.

- Choosing very high deductibles without a claim plan: lower premiums do not help if the deductible is unaffordable later [7].

- Keeping full coverage on an older car automatically: that may not always be cost-effective [7] [8].

- Thinking state minimum liability and full coverage are the same thing: they are not [6].

Key Takeaway

Affordable full coverage car insurance is really about balance. The best policy is not always the absolute cheapest one and not always the most loaded one. It is the full coverage setup that protects what matters, keeps the deductible realistic, and stays manageable over time.

Frequently Asked Questions

Is full coverage an official insurance product?

No. It is usually a common phrase for a policy that includes liability plus collision and comprehensive, along with any other required coverages [1] [2].

Why is full coverage usually more expensive than liability-only?

Because it generally protects more risks, including damage or loss involving your own vehicle, not just damage you cause to others [3] [4].

Can I make full coverage more affordable without giving it up completely?

Often yes. Comparing insurers, choosing deductibles carefully, and reviewing the vehicle’s value can all help lower costs [7] [8].

Do financed cars usually need full coverage?

In many cases, lenders require collision and comprehensive on financed or leased vehicles [4].

What if I only want the cheapest legal option?

Then your better starting point may be cheap liability car insurance, because that page is focused on lower-cost liability-only coverage instead of broader protection.

Final Thoughts

Affordable full coverage car insurance is possible, but the best result usually comes from making smart tradeoffs instead of chasing the lowest number blindly. Full coverage can be worth the extra cost when the vehicle matters enough that losing it would create real financial stress.

The key is to compare carefully, understand what full coverage actually means, and shape the policy so the protection is still affordable at startup and over time.

Compare Broader Protection More Clearly

Start with the page that fits your situation, understand how upfront costs work, and compare whether liability-only or fuller protection makes more sense for your vehicle and budget.

References

- Progressive – What Is Full Coverage Car Insurance? ↩ Back to section

- Progressive – Liability vs. Full Coverage Car Insurance ↩ Back to section

- Insurance Information Institute – What Is Covered by a Basic Auto Insurance Policy? ↩ Back to section

- NAIC – Auto Insurance ↩ Back to section

- Insurance Information Institute – Collision and Comprehensive Coverage ↩ Back to section

- NAIC – A Consumer’s Guide to Auto Insurance ↩ Back to section

- Insurance Information Institute – Nine Ways to Lower Your Auto Insurance Costs ↩ Back to section

- NAIC – Tips for Saving on Your Auto Insurance ↩ Back to section