If you need car insurance and your credit is not in great shape, the first problem is often not just the total premium. It is the amount due today. Many drivers in this situation are not only trying to find affordable coverage over time. They are trying to get insured now without a heavy upfront payment.

That is exactly where bad credit car insurance with low down payment becomes relevant. In many cases, you can still get coverage with a manageable first payment, but you may need to compare more carefully, keep your policy simple, and understand how insurers use credit-based insurance scores in states where that practice is allowed [1] [2].

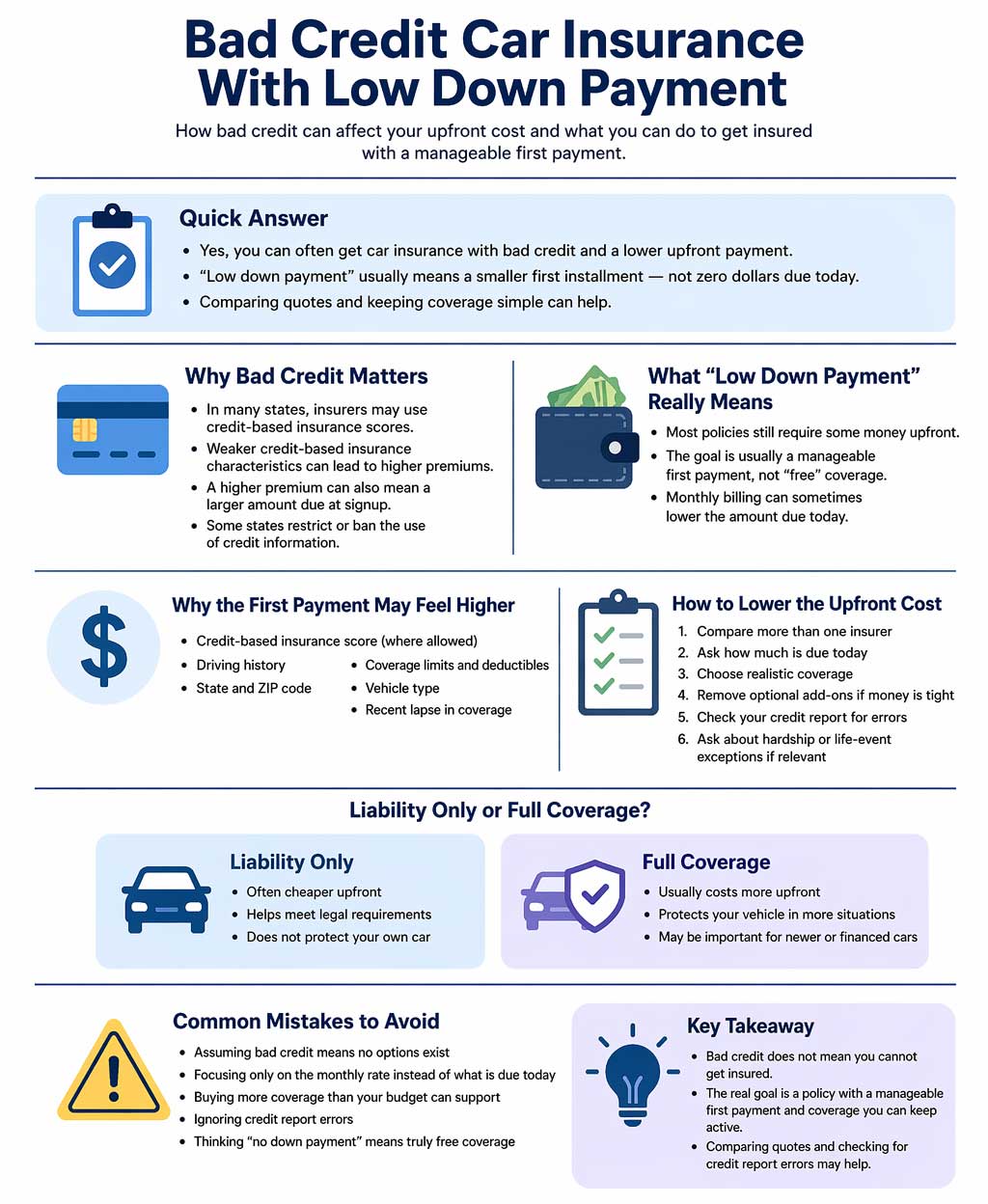

Quick Answer

Yes, you can often get car insurance with bad credit and a lower upfront payment, but you should not expect true free coverage at signup. In practice, low down payment usually means a smaller initial installment rather than zero dollars due today [5].

Why Bad Credit Can Affect Car Insurance

Many drivers assume insurers look only at accidents, tickets, and the type of vehicle you drive. Those things do matter, but in many states insurers may also use a credit-based insurance score in underwriting and rating. That score is not the same thing as your regular consumer credit score, even though it draws on information from your credit report [1] [2].

The practical result is simple: if your credit-based insurance characteristics are weaker, your premium may be higher. That can also make the first payment harder to manage, especially if the insurer wants more money upfront before the policy starts [2] [3].

Some states restrict or ban how insurers use credit information, so this factor is not treated the same way everywhere [1] [3]. But for many drivers, bad credit can still be one reason a quote feels more expensive than expected.

If you want the broader explanation of how low upfront cost insurance works, see what no down payment car insurance really means.

What Low Down Payment Really Means When You Have Bad Credit

This part is important. Most drivers searching for bad credit car insurance low down payment are not actually looking for a magical policy with nothing due today. They are usually looking for a policy that starts with a smaller first payment and then spreads the rest across installments.

That distinction matters because true no down payment car insurance is generally not a standard product. Most policies still require some money upfront, often the first month, a portion of the premium, or another initial charge [5].

So the goal is usually not to find a policy with zero startup cost. The goal is to find one where the first payment is realistic for your budget while still keeping you legally insured and helping you avoid a lapse.

Why the First Payment May Feel Higher With Bad Credit

Bad credit does not automatically mean you cannot get insured. But it can make the numbers harder to manage. When the premium goes up, the startup cost often becomes the part that hurts most.

That first payment can feel higher because several pricing factors may be working together at the same time:

- Your credit-based insurance score where allowed

- Your driving history

- Your ZIP code and state rules

- The car you want to insure

- Your coverage limits and deductibles

- Whether you need continuous coverage right away after a recent gap

If you recently lost coverage after missing payments or canceling a policy, that can add another layer of cost. In that case, you may also want to read car insurance after a lapse with low down payment.

Can You Still Get Covered With Bad Credit?

Yes. Bad credit can make insurance more expensive, but it does not mean you are uninsurable. The better question is how to structure the policy so the first payment is manageable and the coverage is realistic for your situation.

For many drivers, the best move is to compare multiple quotes, avoid unnecessary extras, and choose a coverage setup that balances legal protection with affordability. That can mean starting with liability-only coverage if your situation allows it, then upgrading later when your budget improves.

How to Lower the Upfront Cost

If you are trying to keep the first payment down, these are usually the most practical moves:

1. Compare more than one insurer

Two companies can view the same driver very differently. That matters even more when credit is part of the pricing picture.

2. Ask exactly how much is due today

Do not focus only on the advertised monthly premium. The amount due at signup is what matters if cash is tight.

3. Keep coverage realistic

Choose the protection you truly need right now. A policy is only useful if you can afford to keep it active.

4. Review optional add-ons

Rental reimbursement, roadside assistance, and similar extras can be useful, but they can also increase what you owe upfront.

5. Check your credit report for errors

If there is inaccurate information on your credit report, disputing it may help over time. You can get free credit reports through the official federally authorized site, and the CFPB explains how to dispute errors with the credit reporting company [6] [7].

6. Ask about hardship or life event exceptions if relevant

The NAIC notes that if a hardship affected your credit history, you can ask your insurer whether it will consider a life event exception [3].

If you want a more general comparison of lower-upfront-cost policies, see low or no down payment car insurance and cheapest car insurance with low down payment.

Should You Choose Liability Only or Full Coverage?

This is where a lot of drivers with bad credit have to make a practical decision. If affordability is the main issue, liability-only coverage may be the easiest way to restart or maintain insurance because it is often cheaper than full coverage.

But cheaper is not always better. If your car is newer, financed, or difficult to replace, broader coverage may still make more sense even if the first payment is higher. The key is making a choice based on your actual risk, not just on the cheapest quote in front of you.

Key Takeaway

If bad credit is pushing your quote up, the most realistic goal is usually not zero down. It is finding a policy with a manageable first payment, the right minimum level of protection, and a setup you can keep active without another lapse.

Common Mistakes to Avoid

Drivers with bad credit often make the same mistakes when trying to lower insurance costs fast:

- Assuming bad credit means no options exist: coverage is often still available, but shopping carefully matters.

- Focusing only on the monthly number: the amount due today is the real budget test.

- Buying too much coverage for the current budget: an unaffordable policy can lead to another lapse.

- Ignoring credit report errors: inaccurate information can hurt you unnecessarily [7].

- Thinking no down payment means truly free coverage: it usually does not [5].

Frequently Asked Questions

Does bad credit always raise car insurance rates?

Not always in the same way everywhere. In many states, insurers may use credit-based insurance scores, but some states restrict or ban that practice [1] [3].

Can I get low down payment car insurance with bad credit?

Often yes. But low down payment usually means a smaller first payment, not zero dollars due at signup [5].

Is a credit-based insurance score the same as my regular credit score?

No. They are related, but they are not the same thing. Insurers may use a credit-based insurance score rather than a standard consumer lending score [1] [2].

Can fixing credit report errors help over time?

It can. The CFPB recommends disputing inaccurate information with the credit reporting company and providing supporting documents when needed [7].

What if I just want the cheapest possible option right now?

Then it usually makes sense to compare a simpler liability-focused policy first and review lower-cost provider options. You can start with best low down payment car insurance companies.

Final Thoughts

Bad credit car insurance with low down payment is possible, but the best results usually come from a practical approach. Compare several quotes, focus on the amount due today, keep coverage realistic, and do not assume the first offer is the only one available.

If your goal is to get insured now without overloading your budget, a lower initial payment and a policy you can actually maintain are usually more important than chasing the idea of perfect zero-down coverage.

References

- NAIC – Credit-Based Insurance Scores ↩ Back to section

- NAIC – Credit-Based Insurance Scores Aren’t the Same as a Credit Score ↩ Back to section

- NAIC – A Consumer’s Guide to Auto Insurance ↩ Back to section

- Insurance Information Institute – Nine Ways to Lower Your Auto Insurance Costs ↩ Back to section

- ValuePenguin – Cheap No Down Payment Car Insurance ↩ Back to section

- AnnualCreditReport.com – Official Site Information ↩ Back to section

- CFPB – How Do I Dispute an Error on My Credit Report? ↩ Back to section