If your goal is to get insured without paying for more coverage than you need, cheap liability car insurance is often the first place to look. For many drivers, liability-only coverage is the simplest path to legal driving status and a lower premium than a broader policy with collision and comprehensive protection.

That said, cheap does not mean careless. Liability insurance is designed to help pay for injuries or property damage you cause to other people, but it usually does not pay to repair your own car after a crash [1] [2] [3]. That is why the cheapest liability policy is not always the right choice for every driver.

Quick Answer

Cheap liability car insurance usually means a policy focused on the state-required liability coverages, often with no collision or comprehensive added. It can be one of the most affordable ways to get insured, but you still need to compare startup cost, policy limits, and whether minimum coverage is truly enough for your situation [1] [4] [5].

What Cheap Liability Car Insurance Actually Means

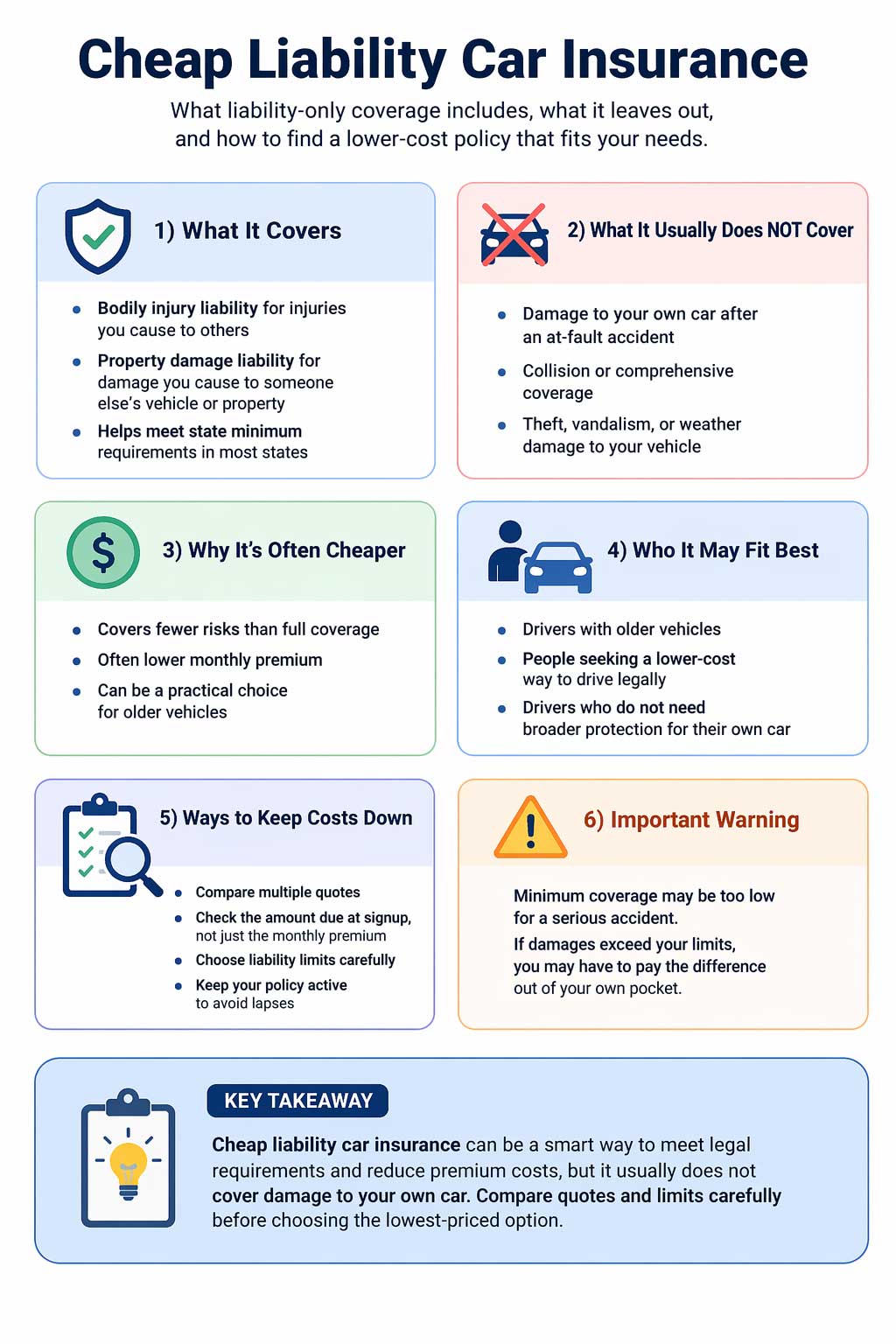

Liability-only car insurance is usually the leanest standard auto policy a driver can buy. In most states, you need some level of bodily injury liability and property damage liability to drive legally [1] [6]. Bodily injury liability helps pay for injuries you cause to others. Property damage liability helps pay for damage you cause to someone else’s vehicle or property [1] [2].

When drivers search for cheap liability car insurance, they are usually trying to do one or more of these things:

- lower the monthly premium

- reduce the amount due at signup

- meet legal requirements quickly

- avoid paying for full coverage on an older vehicle

If you want the broader explanation of lower upfront cost policies, you can also read low or no down payment car insurance and what no down payment car insurance really means.

What Liability Insurance Covers

The core of a liability-only policy is protection for the damage you may cause to other people. That usually includes:

- Bodily injury liability: medical costs, and in many cases related losses, for people injured in an accident you caused

- Property damage liability: repairs or replacement costs for another person’s vehicle or other property you damage

That is why liability insurance matters even for drivers focused mainly on affordability. It may not protect your own car, but it can help protect you financially if you cause a serious loss for someone else [2] [7].

What It Usually Does Not Cover

This is where many drivers make the wrong assumption. Liability-only coverage generally does not pay for damage to your own vehicle after an at-fault accident. It also does not automatically include broader protections commonly associated with a fuller policy, such as collision and comprehensive coverage [3] [8].

That matters because the cheapest liability quote can look appealing right away, but if you drive a newer car, owe money on the vehicle, or cannot afford to replace it after a crash, a bare-bones policy can leave you exposed.

Why Liability-Only Coverage Is Often Cheaper

Liability-only coverage is often the cheaper route because it insures fewer risks than a broader policy. When you leave out collision and comprehensive, the insurer is generally not agreeing to pay for damage to your own car in the same way it would under a fuller policy [3] [8].

But cheaper is still relative. The amount you pay can change based on:

- your age and driving record

- your ZIP code and state

- the vehicle you drive

- the liability limits you choose

- whether you have a recent lapse

- whether credit-related insurance factors affect pricing in your state

If weak credit is also part of your situation, see bad credit car insurance with low down payment. If your previous policy ended, see car insurance after a lapse with low down payment.

Why the State Minimum Is Not Always Enough

One of the biggest mistakes drivers make is assuming that the legal minimum must also be the smart amount to buy. The NAIC notes that state minimum liability limits can be too low to fully protect you after a serious accident [4]. If damages go beyond your policy limits, you can still be financially responsible for the amount above them [5].

So if you are shopping for cheap liability car insurance, the best strategy is usually not just “buy the absolute minimum.” It is “buy the lowest-cost liability policy that still makes sense for your real risk.”

How to Find Cheap Liability Car Insurance Without Making a Bad Choice

If affordability is the main goal, these are the smartest moves:

1. Compare several quotes

Even for liability-only coverage, insurers can price the same driver very differently. That is one reason comparison shopping matters so much [4].

2. Check the amount due today

Do not focus only on the monthly premium. Some policies look cheap monthly but still require a higher startup payment than expected.

3. Choose limits carefully

Buying the absolute minimum can save money today, but it may leave you exposed later if you cause a larger loss [4] [5].

4. Avoid paying for coverage you do not need

If your vehicle is older and not worth much, liability-only may be more reasonable than a broader package. But that depends on your ability to absorb a loss if the car is damaged.

5. Keep the policy active

Allowing coverage to lapse can make future quotes harder to manage. If timing matters, read same-day car insurance.

Who Cheap Liability Car Insurance Fits Best

Cheap liability-only coverage may make sense for drivers who:

- drive an older vehicle with limited value

- want a lower-cost way to meet legal requirements

- need a practical short-term budget solution

- do not have a lender requiring broader coverage

It may be a poor fit for drivers who:

- have a newer or financed vehicle

- would struggle to replace their car after a crash

- want more complete protection instead of the lowest possible premium

Common Mistakes to Avoid

- Thinking liability covers your own car: it usually does not [3].

- Buying only by monthly price: startup cost matters too.

- Assuming state minimums are automatically enough: they may not be [4].

- Ignoring your real vehicle value and risk: cheap coverage is only useful if it fits your situation.

- Letting the policy lapse: that can make future shopping harder.

Key Takeaway

Cheap liability car insurance can be the right move when your priority is legal driving status and a lower premium. But the best policy is not always the absolute cheapest one. The smarter goal is affordable liability coverage with limits and startup costs that still make sense for your situation.

Frequently Asked Questions

Is liability-only car insurance the cheapest kind of car insurance?

Often yes, because it usually provides less protection than a broader policy that also covers damage to your own vehicle [3] [8].

Does cheap liability car insurance cover my own car?

Usually no. Liability coverage generally pays for injuries or property damage you cause to others, not damage to your own vehicle [1] [3].

Should I buy only the state minimum?

Not automatically. State minimums can be too low for a serious accident, so the cheapest legal option is not always the safest financial choice [4].

Can I get cheap liability insurance with a low down payment?

Often yes, but the amount due at signup still varies by insurer, state, and driver profile. If that is your main concern, start with low or no down payment car insurance.

What if I mainly want to compare providers?

Then the best next page is best low down payment car insurance companies.

Final Thoughts

Cheap liability car insurance can be a smart solution when you want to control costs and meet legal requirements without paying for a broader policy than you need. The key is knowing exactly what liability covers, what it leaves out, and whether the lower price matches your actual risk.

If your goal is simple affordability, liability-only may be a practical place to start. But if you want broader protection, faster coverage, or help with a more specific situation, the right next page may be different.

Compare Low-Cost Options More Clearly

Start with the page that fits your situation, review how upfront costs work, and compare affordable policy types before you choose the lowest-priced option.

References

- NAIC – Auto Insurance ↩ Back to section

- Progressive – Auto Liability Coverage ↩ Back to section

- Insurance Information Institute – What Is Covered by a Basic Auto Insurance Policy? ↩ Back to section

- NAIC – A Consumer’s Guide to Auto Insurance ↩ Back to section

- NAIC – Consumer Shopping Tool for Auto Insurance ↩ Back to section

- Insurance Information Institute – Automobile Financial Responsibility Laws by State ↩ Back to section

- Insurance Information Institute – Auto Insurance Basics ↩ Back to section

- Progressive – Liability vs. Full Coverage Car Insurance ↩ Back to section